The last few months’ cascade of failures by centralised projects serving the crypto market highlighted both the power of decentralised transparency and point to weaknesses in the regulatory approach to date that can inform future regulation. We explore what failed, if CeFi can be trusted and what kind of regulation achieves the best investor protection.

Crypto didn’t fail -centralised corporations servicing the crypto market failed

Contagion from the failures in the centralised finance sector that started in June seems to have continued with the failure of FTX/Alameda. These losses from a few months ago look to have been papered over and only became apparent in the last week after leaked internal financials were published in the crypto press. Now further contagion from the collapse of a major exchange becomes a possibility.

Trust in the crypto market has undoubtedly been shaken by the events of the last few months, and especially so by the recent collapse of FTX – the second largest crypto exchange, with a history of extraordinarily successful fundraising rounds, powerful backers, fast business volume growth, and a high profile CEO with strong regulatory and political connections.

As the market digests the shock of the apparent deception behind the facade of comfortable financial stability and the respectability gained from advocating for transparency and more regulation, it is important to pick apart what failed, and what did not.

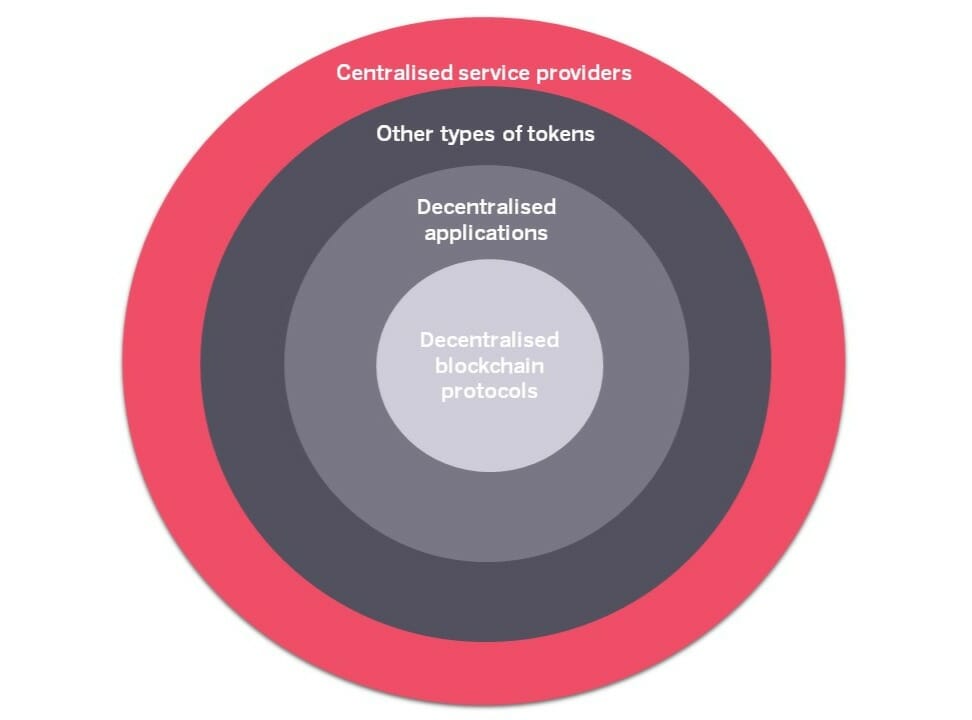

At its heart, the crypto market is a universe of decentralised blockchain protocols that multiple use cases, applications, and token types can build on. None of this has changed and none of this has failed.

Crypto projects continue building and innovating around the remaining technological limitations and challenges. Meritless blockchain protocols are easy to identify as they will have no technological advantage and/or no ecosystem of projects building on them. All this information is transparent.

The tokens of technologically meritless projects can still appreciate (eg Dogecoin) and create the risk of serious investment losses – but none of the risks are hidden. Other projects may in the end deliver less than hoped or fail to gain adoption, but in such cases, any losses to tokenholders would be normal investment losses – the investor took a view on a project and the outcome turned out differently.

It was neither blockchain protocols nor decentralised applications built on these blockchains that misused customer funds or took excessive non transparent risks. Ironically, it was centralised businesses that caused damage to the decentralised crypto ecosystem.

While decentralised blockchain projects build, their tokens are often traded, custodised, lent, borrowed, and invested in by an ecosystem of centralised finance companies – exchanges, lenders, banks and custodians. The vast majority of these are private and many operate in weak jurisdictions . They are no different from traditional financial service providers, and because most of them are private, they operate with low transparency. It was these centralised financial service providers that provided a string of shocks this year, with misuse of customer funds, extraordinarily risky business practices, and misrepresentations.

It is important to remember that cryptocurrencies don’t require centralised intermediaries – investors and users can directly interact with the projects and their tokens on the blockchain. There are also decentralised alternatives to the centralised service providers. However, many prefer the convenience of interacting with the crypto market through centralised financial institutions, and for institutional investors it is often a necessary requirement to perform Know-Your-Customer (KYC) and Anti Money Laundering (AML) checks to access crypto asset investments.

Meanwhile the decentralised blockchain ecosystem continued operating transparently and as intended. Crypto didn’t fail. Certain bad (or reckless) actors providing pipes to the crypto market failed. The decentralised projects at the heart of crypto will carry on building.

Decentralisation wins

The answer the crypto industry offered to the question of how to guarantee trust was to build trustless, decentralised systems. And while decentralisation is not the only solution, it is a very good, very robust solution.

With all transactions transparently recorded on the blockchain, decentralised finance projects operated as normal. No hidden risks were – or ever could be – taken by these platforms.

An example is the contrast between decentralised credit lending platform Maple Finance and centralised lender Celsius. Lenders using the Maple platform take credit risk on the borrowers, however, they do so knowingly and by choice. Celsius depositors did not know that their funds were lent out with credit risk on the borrowers or used in highly levered bets.

Can CeFi be trusted?

Many of the centralised finance businesses servicing the crypto market are trustworthy and operate with high integrity. However, the lack of transparency makes it difficult to determine which entities merit trust.

The crypto market is responding to this challenge in a typical antifragile fashion, by some CeFi entities offering a great degree of voluntary, self-imposed transparency that is otherwise not required of them, being private corporations. This will allow the market to channel their business to entities that are providing valid proof points of the integrity of their business practices and avoid the rest – the crypto market de facto self-regulating.

Such self-regulation is in many ways more powerful than imposed regulation because the latter is a game of cat and mouse, with an expensive overhead. When the market chooses to embrace certain high integrity practices, it makes it easy for market participants to separate the wheat from the chaff without having to rely on the endorsement of other credible parties. The FTX crisis has shown that such endorsements do not necessarily mean much.

In some ways, the collapse of FTX was the crypto market ridding itself of bad actors in the interest of the medium to long term health and growth of the industry.

Regulatory arbitrage

Crypto regulation has been on the agenda in most Western countries, and regulators are bound to respond to the current events with proposing more regulation, more enforcement actions, and possibly an accelerated timeline for enacting new rules.

This in some ways is a positive for the crypto market as regulatory uncertainty has driven a lot of businesses (including FTX) to weak jurisdictions where abuses are likelier to occur. This is especially so when lack of clear ante facto rules are combined with post facto enforcement action such as prosecuting tokenholders who voted in a DAO (decentralised autonomous organisation).

At the same time, excessive regulation can also (and already has) driven some crypto businesses to weak jurisdictions. Imposing costly overheads that make it difficult for young businesses to break even, or that severely limit their opportunities, means that these companies are likely to keep seeking jurisdictions where they are able to operate and grow. This in turn increases the risk of abuses and poor business practices. The end result may be that the overly stringent regulation will actually make the industry riskier, not safer.

The path towards trust

As the traumatic events unfold, it is important to recognise that the reckless or fraudulent business practices that are being exposed were not carried out by decentralised projects but by private corporations – mostly located in weak jurisdictions – that provided financial services to investors who don’t want to directly interact with the decentralised platforms.

The lack of transparency of centralised business models has been shown to be inferior to the decentralised transparent model that is the essence of crypto and the very innovation the industry is built on.

Credible, high integrity centralised entities in the crypto market are responding with voluntary transparency and self-regulation. Meanwhile, the hope is that regulation will take a constructive path – offering clarity, providing protection, but remaining proportionate so as not to continue driving crypto businesses into risky jurisdictions.

To be the first to get the latest news on Sygnum and the market, expert insights and industry research please follow us on Linkedin and Twitter.

About Sygnum

Sygnum is the world’s first digital asset bank, and a digital asset specialist with global reach. With Sygnum Bank AG’s Swiss banking licence, as well as Sygnum Pte Ltd’s capital markets services (CMS) licence in Singapore, Sygnum empowers institutional and private qualified investors, corporates, banks, and other financial institutions to invest in the digital asset economy with complete trust. Sygnum operates an independently controlled, scalable, and future-proof regulated banking platform. Our interdisciplinary team of banking, investment, and Distributed Ledger Technology (DLT) experts is shaping the development of a trusted digital asset ecosystem. The company is founded on Swiss and Singapore heritage and operates globally. To learn more about Sygnum, please visit www.sygnum.com.

Disclaimer

This information was prepared by Sygnum Bank AG. This information may contain forward looking statements and may be subject to change. The opinions expressed herein are those of Sygnum Bank AG, its affilitates, and partners at the time of writing. This is for informational purposes only and contains general material. It does not constitute any advice or recommendation, an offer or invitation by or on behalf of Sygnum Bank AG to purchase or sell assets or securities. It is not intended to be used as a general guide to investing, and it should be used for informational purposes only. When making an investment decision, you should either conduct your own research and analysis or seek advice from an expert to make a calculated decision. The information and analysis contained here have been compiled from sources believed to be reliable. However, Sygnum Bank AG makes no representation as to its reliability or completeness and disclaims all liability for losses arising from the use of this information.

Sign up for Future Finance

Join our 40,000 strong global community to future proof your investments. Sign up now to be the first to receive our news, product launches, industry reports and educational series.