After isolated examples in the past, 2021 saw the beginnings of a trend towards mergers and acquisitions (M&A) activity in the crypto asset market. In this article, we consider what M&A mean in practice in the crypto space, and whether the trend is likely to continue.

The rationale

The reasons for mergers and acquisitions for blockchain projects are similar to those that apply for traditional companies: faster business build, strategic synergies, achieving critical mass to compete, diversification, sharing overhead and horizontal or vertical integration. To execute a token merger or acquisition in practice, the mechanics of token migration (a new token inherits the balances of the old token) or token swaps can be applied.

Despite the rationale and the mechanics in place, it was not until last year that token merger and acquisition activity started to grow. One possible reason may be the increased complexity associated with token mergers.

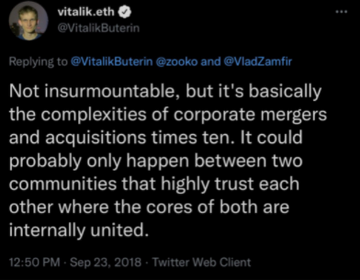

Vitalik Buterin (founder of Ethereum) in 2018 on the possibility of crypto mergers

M&A attempts to date

2017 – the spoon

The spoon was conceptualised in 2017 and first implemented in 2018 and could be described as the first attempt at a crypto M&A. This involved combining the capabilities of two blockchains by “spooning” the balances onto another chain to create a best-of-both-worlds protocol. Examples include the replicated Ethereum on Cosmos (Ethermint) and on Avalanche (Athereum).

2018 – access to treasury funds

In 2018 in the aftermath of the initial coin offering (ICO) boom, proposals were floated for the first financially motivated token mergers. The idea was to combine the often substantial funds raised that remained largely unspent with the projects not progressing during the Crypto Winter, and join forces to get languishing projects over the line.

2019 – the first token merger

The first token merger happened in 2019 with a small merger between two struggling projects. This merger, valued at USD 5 million, between the centralised exchange COSS and the crypto payments provider LaLa World intended to combine resources and provide an integrated solution. The COSS and LALA tokens were swapped for a newly created token. The project, however, continued to struggle.

2020 – the first acquisition

The first landmark crypto M&A deal was the acquisition by crypto broker Voyager (with its VGX token) of the French crypto exchange LGO. The agreement was completed at the end of 2020, and the USD 900 million token swap happened in August 2021. The VGX and LGO tokens were combined into a new version of the VGX token. The primary goal of the merger was geographic expansion, and both tokens rallied 25-fold between the announcement and the eventual token merger.

2021 – the first hostile takeover?

M&A activity picked up in 2021, with several projects including a landmark acquisition by Polygon, the USD 800 million Rari Capital-Fei Protocol token merger, two data privacy projects (KEEP and NuCypher) joining forces, and what some termed as a hostile takeover of the xDAI Chain by Gnosis.

Polygon is successfully executing a fast-paced strategy towards offering a full range of blockchain scaling solutions. It has been using tokens from its treasury to acquire technologies such as Hermez’s Zero Knowledge rollup technology (swapping HEZ tokens for Polygon’s MATIC tokens).

Meanwhile, the treasury tokens of stablecoin project Fei Protocol (TRIBE) will be swapped for yield farming protocol Rari Capital’s RGT tokens in a strategy that aims to create a full-service decentralised finance infrastructure. With this merger, the combined platform will have USD 2 billion in total value locked (TVL), helping two mid-size decentralised finance (DeFi) projects reach critical mass.

Well-connected and well-funded DeFi platform Gnosis is swapping treasury tokens (GNO) worth about USD 150 million for xDai Chain’s tokens (STAKE) to acquire a layer 1 protocol, now renamed the Gnosis chain. Despite being well regarded, xDai has been struggling to compete in the crowded layer 1 protocol space without a well-funded treasury. Although the terms of the Gnosis offer give xDAI token holders a premium, the community around the smaller project still felt hard done by and alleged a “hostile takeover”.

The USD 900 million merger announced between the KEEP Network and NuCypher, completed at the start of 2022, will combine the platforms and create a new token. The projects are seeking critical mass through the merger instead of competing with similar offerings for the same client base. Token holders of the two projects receive an equal share of the tokens of the newly created platform, the Threshold Network.

Non-merger mergers

Some token mergers consolidate multiple tokens issued by the same project. An example is crypto.com merging their MCO tokens issued in their original 2017 ICO into the native token of their blockchain, CRO, to simplify and consolidate their token structure. This does not involve any change in the operations of the platform, but it alters the economics for the token holders.

Some crypto projects are quite liberal with the use of the term “merger”. For example, Yearn refers to strategic alliances and joint ventures as mergers. These tie ups tend to involve the merger of some technologies or resources but not the tokens or the governance.

Will the trend continue?

There are certain obstacles specific to the crypto market that slow the trend:

- Decentralised projects can lack coherent strategic vision

- Strong communities and tribalism can stand in the way of acceptance of a merger

- Acquisitions require a well-funded treasury, which many projects do not have

- Merging the disparate governance mechanisms of different DAOs can be a serious challenge

- As crypto assets are typically highly volatile, especially for small or medium-size tokens, the relative market capitalisation of two projects with a good strategic fit can change dramatically over relatively short periods, making it difficult to reach an agreement on the terms that both projects’ token holders could be comfortable with

In a fast-growing industry, the mentality “there is room for us all” tends to dominate. However, at this point, there is significant rationale for token mergers in more mature sectors of the crypto market, such as the protocol layer and decentralised finance, as they become increasingly competitive. Achieving critical mass, pooling resources and exploiting synergies from horizontal or vertical integration are strategically compelling and we expect to see much more M&A activity.

To be the first to get the latest news on Sygnum and the market, expert insights and industry research please follow us on Linkedin and Twitter.

Disclaimer

This document is purely for educational purposes and has been issued by Sygnum Group. It is not intended for distribution, publication, or use in any jurisdiction where such distribution, publication, or use would be unlawful, nor is it aimed at any person or entity to whom it would be unlawful to address such a marketing communication. It does not constitute an offer or a recommendation to subscribe, purchase, sell or hold any security or financial instrument. It contains the opinions of Sygnum Group, as at the date of issue. These opinions and the information contained herein do not take into account an individual‘s specific circumstances, objectives, or needs. No representation is made that any investment or strategy is suitable or appropriate to individual circumstances or that any investment or strategy constitutes personalized investment advice to any investor. Therefore, you must verify the above and all other information provided in the document or otherwise review it with your external advisors. Some investment products and services, including custody, may be subject to legal restrictions or may not be available worldwide on an unrestricted basis. The information and analysis contained herein are based on sources considered as reliable. Sygnum Group uses its best efforts to ensure the timeliness, accuracy, and comprehensiveness of the information contained in this document. Nevertheless, all information indicated herein may change without notice.